Disability coverage advantages in uncertain financial times

By: Benefits by Design | Tuesday May 13, 2025

Updated : Monday May 12, 2025

The disability coverage advantages for both employers and employees are varied, but not uncomplicated. Managing future expectations regarding trade tariffs and therefore retails costs is on all our minds, whether you are in an affected industry or not. Prudency has led us to review our safety nets, and that includes employee benefits.

The business case for disability coverage

Disability coverage advantages for employers are often underestimated.

Firstly, having a plan that meets their needs improves employee loyalty. Employees rank their benefits plan as the #2 reason (after salary) for staying with a company.

Moreover, replacing a high-level employee costs over 200% of their annual salary. This includes loss of institutional knowledge and expertise. That’s 10x more than replacing an entry-level employee. Another reason to ensure your top talent is happy with the current benefits plan.

Tough choices in uncertain financial times

Many Canadians are feeling anxious about their finances, and a third of them are unable to save for emergencies. Disability coverage is more important than ever in times like these. Being off work due to illness or injury without it could leave some individuals or families unable to pay bills, make rent, or even buy groceries.

Employees are making tough choices, and some could look for work elsewhere if they don’t have the protection they need. In fact, 52% of employees said they were on the lookout for a new job in 2025 because they were unsatisfied with their current company benefits.

Combatting rising disability coverage costs

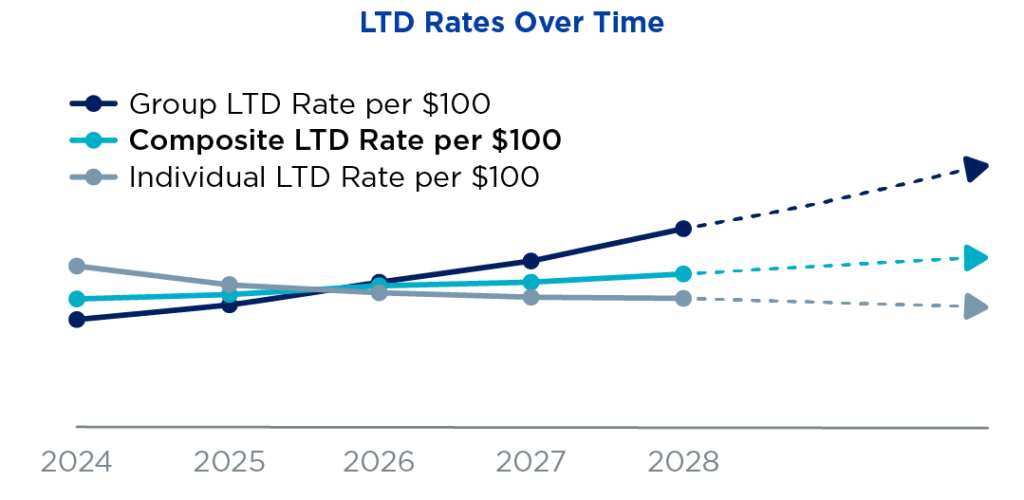

At the same time, the cost of long-term disability (LTD) rates is predicted to rise by 5%-7% in 2025. LTD is usually employee-paid to make the benefit non-taxable. This means employees have skin in the game when it comes to choosing the right coverage.

Rate volatility and annual increases are a risk with traditional group LTD coverage because premiums are based on demographics, claims experience, and external risk factors.

Combo long-term disability insurance plans help by providing a portion of the LTD coverage as individual policies. The premium prices are locked in for the lifetime of the individual policies, which are transportable should the employee leave. Employers can protect their employees with guaranteed long-term rate stability, a major advantage in today’s unstable economy.

Many high earners aren’t fully protected due to benefit maximums and non-evidence thresholds. Another combo disability coverage advantage is the ability to provide coverage above the Non-Evidence Maximum (NEM) for high earning employees.

For example, an employee earning $111,000 could lose over $24,000 in LTD benefits if not properly covered. The downloadable brochure below goes into further detail on how this works.

[DOWNLOAD] Combo long-term disability insurance brochure

Disability coverage advantages

There are some clear advantages to disability coverage, which can and should be elucidated to your employees as often as possible to ensure full understanding. The more employees understand their benefits, the higher the perceived value.

Early intervention

When an employee is off work for an extended period, it can come at more than a monetary price.

This is because the longer someone is away, the more difficult it can be to reintegrate back into their old routines. Plus, the mental health toll can leave some feeling isolated and without purpose.

The sooner an employee is given support, the easier it will be for them to return to work, even if it is with modified duties. Being part of a community, even if it’s co-workers, helps improve social and mental health.

Ongoing support

During the course of a disability claim case managers are in constant contact with the employee (claimant) to keep recovery a priority.

Oftentimes, they will have access to resources and support which can aid the doctors and/or therapists to speed recovery.

Employers are also kept in the loop in case there are any major developments, such as the prospect of them returning to work soon. Keep in mind no medical information is shared with employers, only necessary claim information.

Returning to work

Disability management programs are even more effective at helping employees return to work as soon as possible. From early intervention to ongoing support, some have been known to reduce time off work by almost half.

On average, insurers take 60-70 days to help an employee get back to work. But businesses using the People Corporation short-term absence and disability management services see return-to-work times between 30-40 days.

[DOWNLOAD] Short-term absence and disability management brochure

Disability coverage options

There are different types of coverage for when employees need time off work due to illness or injury. Depending on the length of time, the severity, and the industry risk, different options are available.

- Short-term disability (STD) insurance – covers employees from first day of illness or hospitalization, or seventh day from an injury for a short period, such as a week or two to several months. Many employers choose not to provide STD coverage in lieu of Employment Insurance. However, the benefit amounts from private plans are usually higher, and employers and employees pay less in EI premiums when certain STD plans are implemented.

- Short-term absence and leave management – helps employees return to work faster through early intervention and ongoing support.

- Long-term disability (LTD) insurance – covers employees whose sickness or injury results in a disability which affects their ability to perform the duties of their current occupation.

- Combo LTD coverage – works in tandem with the traditional LTD coverage above, but provides transportable coverage at guaranteed rates for life.

- Accident and serious illness disability (ASID) insurance – created for to cover employees in high-risk industries. The hybrid nature of ASID insurance provides monthly indemnity payments (like LTD), but only for specific covered conditions or serious injury (like AD&D).

Looming uncertainties from our neighbour to the south have put Canadians in a precarious position. Employers can provide employees with some peace of mind by making sure the disability coverage in place is working effectively for both you and your employees.

![[FREE DOWNLOAD] Group insurance Quick Tax Facts Guide for 2026](https://www.bbd.ca/wp-content/uploads/2026/02/Group-insurance-Quick-Tax-Facts-Guide-for-2026-Banner.webp)