Addressing the Troubling Trend of Rising Disability Claims in Canada

By: Benefits by Design | Tuesday January 26, 2021

Updated : Monday June 20, 2022

Over the last few years, a troubling industry trend has become clear: more Canadians are going on disability. Alongside this comes necessary updates to Insurer’s calculations and rates to keep pace with the rising claims, leading to rising costs.

It’s time to talk about it.

Disability Claims are on the Rise in Canada

The number of Canadians claiming disability insurance, known as the incidence rate, has been increasing year-over-year.

However, this trend of rising disability claims is not unique to BBD. Nor is it seen with any one Insurer, age range, industry, occupation, or province. It is a broad, widespread trend with all evidence pointing to a continuing increase.

In addition, claims are not being resolved at the same pace as new claims are being added. This is resulting in people remaining on disability leave for longer. As more Canadians go on disability leave and stay on it longer, this is leading to more open claims as a whole.

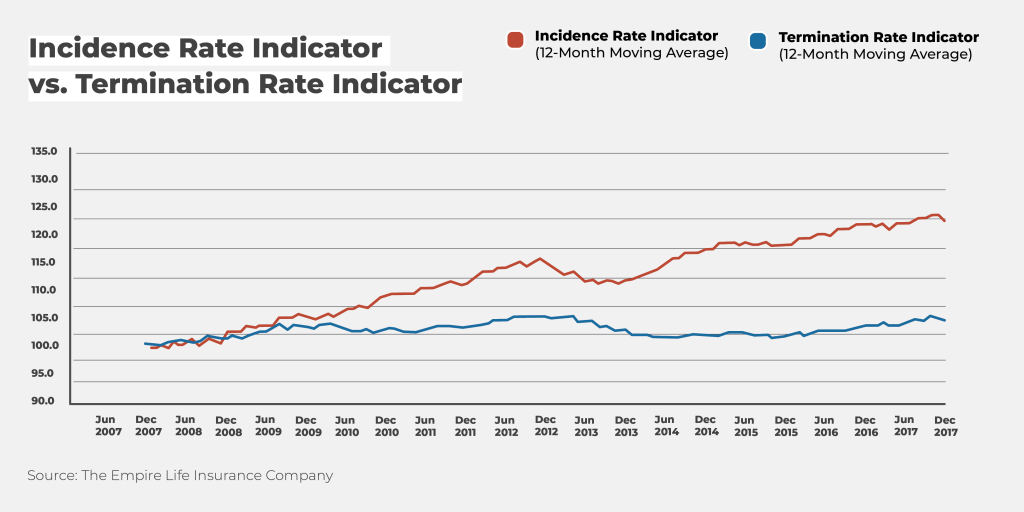

This chart represents data from Empire Life, our Life and Disability Insurance provider. It shows a 12-month average of the rising number of Canadians on their block who go on disability leave (red) next to the relatively stable number of claims that are closed (blue).

Why are Disability Claims in Canada Increasing?

It’s an interesting question, with many possible answers. An aging workforce, deteriorating mental health, low interest rates, reduced workforce, and lack of physical activity among them. But the real answer is: they’re all the right answer because they are all having an impact on disability.

However, we wanted to focus on three: increasing mental health claims, low interest rates, and a reduced workforce.

#1. More Mental Health Claims

According to the Mental Health Commission of Canada, mental health now accounts for 70% of total disability costs, with one in three workplace disability claims in Canada relating to mental illness. There appears to be a couple of reasons for this increase in mental health claims:

COVID-19

The mental health crisis in Canada has worsened during the COVID-19 pandemic. What’s worse, experts expect COVID-19 to continue to impact Canadians’ mental health in the future. This points to a likely continuation of this trend, rather than a reaction to COVID-19 in the moment.

Reduced Mental Health Stigma

Reduced stigma may be further contributing to increases in these kinds of claims as Canadians begin seeking more help. Overall, this is a good thing! But as Canadians become more comfortable talking about their mental health and seeking treatment, increased claims will follow.

The full effects of the reduced stigma and the pandemic on mental health remains to be seen. However, the forecast for Canadians’ mental health in the wake of COVID-19 is almost certainly negative.

#2. Reduced Workforce

Due to layoffs and other work and lifestyle changes, many employers are making do with reduced workforces. This can lead to higher employee turnover and burnout, ultimately flowing through a Long Term Disability (LTD) benefit.

Additionally, returning to work following a disability leave may be growing more difficult in the wake of COVID-19. With reduced doctor visitations, Canadians may have more trouble than before in obtaining their physician’s statements in order to return to work. What’s more, workplaces may be less able to make specific accommodations for workers in order to return to work due to social and physical distancing regulations.

#3. Low Interest Rates

Insurer’s maintain what is called a “reserve fund” for paying claims. Think of it like a pool of money set aside in order to pay Disability claims, all the while collecting interest.

With lower interest rates, Insurers can’t reliably count on that interest earned to pay for any future claims and must therefore set aside more money for the reserve fund. As a result, Insurers are having to account for this declining interest in their calculations, ultimately leading to necessary increases in rates in order to keep everything stable.

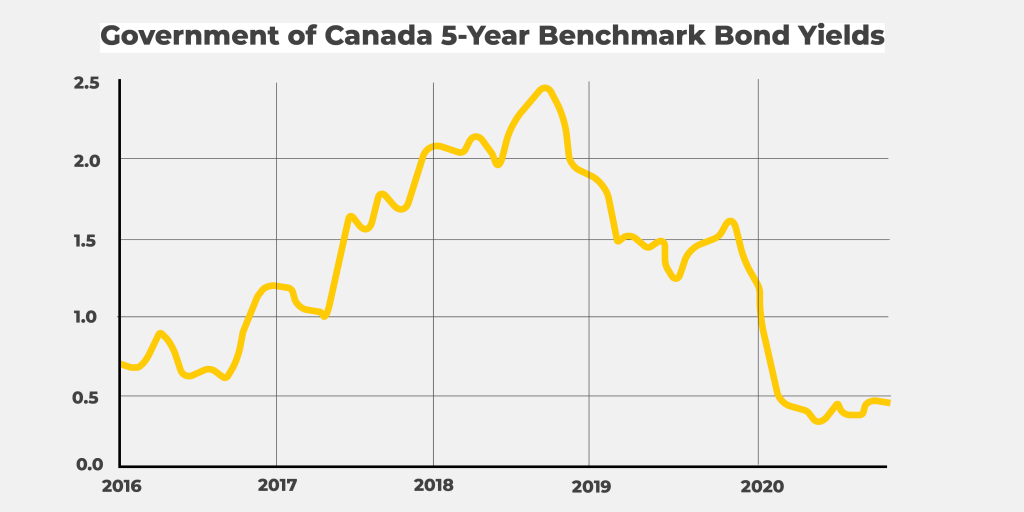

This chart represents data from the Bank of Canada, showing the benchmark bond yields over a 5-year period. You can see the significant drop at the beginning of 2020, however, the trend began in the middle of 2018.

Should Employers Offer Disability Insurance Right Now?

It is true that these rising incidences of disability claims are (and will continue to) lead to an increase in how much Disability Insurance costs. This may lead many employers to wonder if the rising costs of the coverage are worth it.

However, it’s important to remember that the reason the costs are rising is because more and more Canadians are going on disability leave. The likelihood of an employee requiring a leave of absence from work is increasing. Employers who are serious about protecting their employees and supporting them during a necessary leave of absence would do well to consider the merits of Disability Insurance.

Speak with your group insurance Advisor about your options.