Health Care Spending Accounts are here to stay [DOWNLOAD THE 2025 REPORT FREE]

By: Benefits by Design | Tuesday August 19, 2025

Updated : Wednesday October 29, 2025![Health Care Spending Accounts are here to stay [DOWNLOAD THE 2025 REPORT FREE]](https://www.bbd.ca/wp-content/uploads/2025/08/HCSA-Report-Banner.webp)

The 2025 Report: The state of Health Care Spending Accounts by Benefits by Design (BBD) is here! You can read this blog to learn about our overall findings. Download the report for details on how health care spending accounts work, employer quotes, utilization and allotment size graphs and analysis, and more!

2025 Report: The state of Health Care Spending Accounts [PDF: 2.6 MB]

Health care spending accounts are here to stay!

Insurers originally introduced health care spending accounts (HCSAs) as a top-up to traditional insurance. Allowing employers to provide employees with extra protection for medical expenses when they exceed their frequency limits or annual maximums.

For that reason, many employees did not use, or barely used their HCSAs. Many employers and employees were not even aware of their existence, let alone how to use them.

Fast forward to today, and there are groups who solely provide an HCSA as their entire employee benefits package. This category used to mainly consist of groups who were unable to procure traditional, insured benefits. But as employers try to curb benefits spending and stay on budget, this has expanded to all types of group sizes and industries.

On the other hand, companies are also offering HCSAs along with traditional health and dental care benefits — which gives employees more flexibility in how they use their health benefits.

HCSAs allow an employer to see exactly how much they could spend in a given benefit year based on the number of employees and the allocation amounts. Giving employers an exact figure on the maximum amount is extremely attractive, especially given the current financial situation and uncertainty surrounding US tariffs.

Finally, Canadians spent almost $10,000 per person on health expenditures in 2024, and employees are in greater need than ever of extra funds for health care.

How much are employers giving employees?

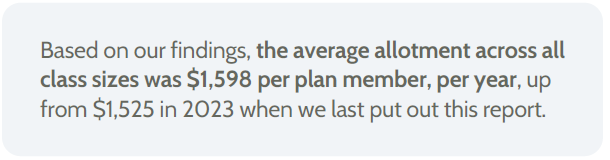

Based on our findings, the average health care spending account (HCSA) allotment was $1,598 per plan member, per year, up from $1,525 in 2023 when we last put out this report.

We broke it down further by class size and found that when there were fewer employees, the allotment was larger. When the class size was between one and four employees, they received almost $2,500. Employees in classes of 5-24 received approximately $1,500, and those with over 25 employees received just $1,200.

We thought this may be indicative of the fact that groups with fewer than 3 employees are often unable to procure traditionally insured benefits, and therefore, the HCSA is their only health and dental benefit. However, when we dug deeper, we found the allotment amounts for groups with other benefits was basically the same as those without other benefits.

Another possibility is that smaller class sizes are comprised of higher-level employees, and employers often offer them more robust benefit packages. Alternatively, when there are more employees, employers may spend less on each one as overall costs increase.

How much are employees using?

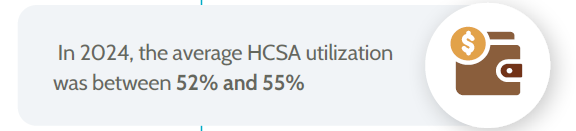

According to our report, in 2024, the average HCSA utilization was 52% (for Standalone HCSAs) and 55% (for GreenShield HCSAs). We also found that when we eliminated those who had not used any amount of their HCSA allotment, utilization for the Standalone groups went up to 59%.

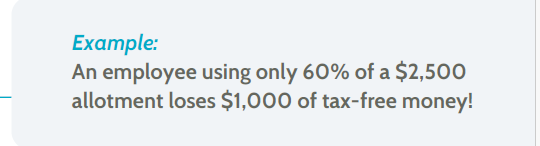

Either way, employees are leaving quite a bit of tax-free money on the table, underscoring the fact that providing these accounts is only the first step. Organizations must show employees when and how to use their benefits if they want them to understand the full value.

[Free Download] How to Nail Your Benefits Communication Strategy

Other benefits of a health care spending account

Here are some more highlights of HCSAs:

- Tax advantages for everyone — claims and fees are tax deductible for the employer, and employees pay no taxes on reimbursements for medical expense claims.

- Ideal for groups ineligible for traditional insurance plans, including

start-ups or high-risk industries.

- Available to any employee earning T4 income, including full-time and part-time.

- No minimum group size, length of time in business, or allotment amounts.

- Companies can choose the pay as you go model — no deposits or pre-funding required.

- Cost-containment — preset amounts make for easy budgeting.

- Employers can mitigate liabilities and remain compliant while saving on administrative costs.

- Organizations can request aggregate claims reports and tax reports.

- Flexible start date and benefits year.

- Employer’s choice of amount, allotment schedule, and rolling type.

It’s clear that HCSAs are here to stay. However, it’s also evident that more work needs to be done when it comes to communicating how they work, how to access them, and what is included in the eligible expenses.

Discover even more about HCSAs – including detailed data analysis and hypotheses

2025 Report: The state of Health Care Spending Accounts [PDF: 2.6 MB]