Group Benefits Plans are an ever-evolving story, and one that should be read frequently. Keeping track of your Claims Experience can help you achieve a sustainable benefits plan that will keep your employees healthy, happy and productive. No-one wants to be surprised by a large increase in premiums come plan renewal time.

Metrics You Should Know to Achieve Sustainable Benefits

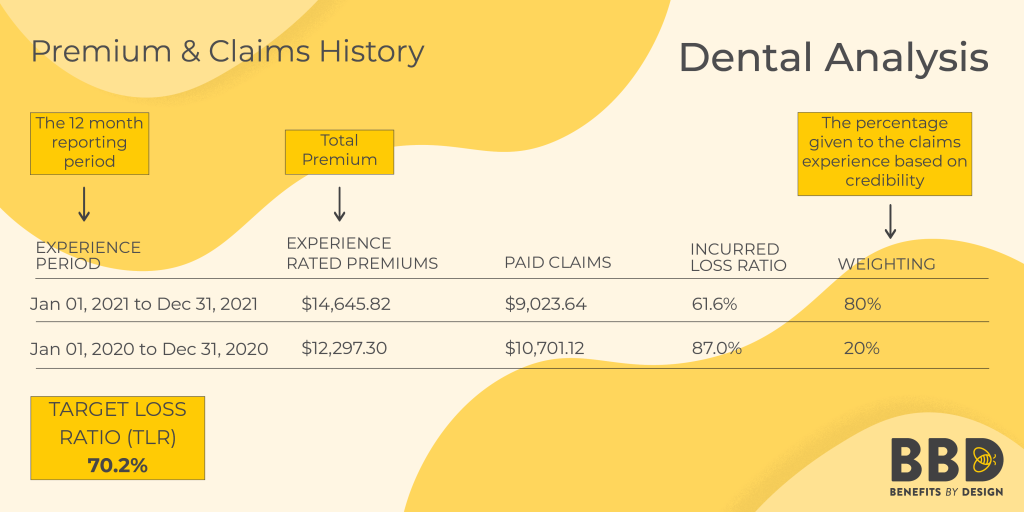

There are a lot of group insurance numbers that are provided in your renewal package. We’re going to focus on the key numbers surrounding Experience Rated Benefits. These include Extended Health Care (EHC), Dental, and Short-Term Disability. They are called experience rated benefits because the premiums are partially based on plan usage – i.e.: experience.

Total Premium

Premiums are the amount the insurer charges for your employee benefits plan coverage. The total premium is the amount paid for the 12 months preceding your renewal.

Paid Claims

How much did your employees use the plan? Paid claims is the total amount of claims paid over the same 12 month period (also known as the experience period) as the Total Premium.

Claims Experience

Your Claims Experience calculates the total Paid Claims versus The Total Premium. It provides the percentage of your premiums that were used by the insurer to pay out claims to your employees.

Target Loss Ratio (TLR)

As the name implies, this is the target percentage your claims experience should be aiming for. This is the percentage that would be available to pay for claims after administration fees, taxes and advisor commissions. The goal is to ensure that your paid claims amount is below your paid premiums amount. Achieving your Target Loss Ratio helps to ensure you do not see an increase in premiums at renewal.

Claims Experience vs. Target Loss Ratio (TLR)

As mentioned above, Target Loss Ratio (TLR) is the percentage of premium that can be paid out in claims. This is the break-even point. Keeping at or below your TLR will help you attain that sustainable benefits plan. If your Dental incurred loss ratio is 70%, and your TLR is 70% you might have a no-change renewal for your Dental coverage. When the claims experience is below the TLR, you might see a slight decrease in premiums. We say might because of other factors which we will discuss.

In the example below, you can see the group was running above target in 2020, and below target in 2021.

Incurred But Not Reported (IBNR)

This refers to claims that a plan member has received the service for (incurred), but they have not yet submitted the claim to the insurer (reported).

If an employee submits a claim several months later, that information would not be available at the time of renewal. Adding an Incurred but not yet Reported amount better reflects the actual total claims experience.

Credibility

The length of time a company has had group insurance for will directly affect how reliable their claims experience history is. Credibility is the percentage that the groups’ own experience will affect the rates when calculating the renewal rates. This percentage increases with the length of time a group remains with a single Insurer, and accumulates faster for groups of a larger size.

For example, it would be hard to determine if, after only 1 year, a group will continue to have low or high claims experience. After 5-10 years, the data becomes much more dependable. A group’s claims experience can thus be analyzed to predict their future usage of benefits, and rates can be set appropriately.

Trend Factors

Trend factors are external elements that are used to calculate standard increases in premiums over time. They include factors such as rising inflation, dental guide fee updates, overall utilization for services, and rising drug costs. The Trend Factors percentage is determined by the credibility of your claims experience.

In other words, if your credibility is low, the Trend Factors will have a higher impact on the outcome of the renewal.

Everything Employers Need to Know About Group Insurance Underwriting

Short-Term Disability Incidence Rate

This refers to the number of employees who were on an approved Short-Term Disability Claim. For example, if 3 employees went on STD during the 12 months preceding the renewal, the incidence rate for STD would be 3. Over time, this number can be used to determine the overall frequency employees might be on approved STD claims, and premiums can be priced accordingly.

Sustainable Benefits Need Communication

Employers can play a proactive role in keeping their employee benefits plan within target. You can request your running claims experience at any time. In fact, your BBD Client Manager will check-in with you every 3 months with an update so you can confirm if you are running above or below target.

Communication is important in employee benefits plans. Both to ensure they are being utilized properly, and so that employees know how to access them should the need arise.

Keep in mind that discussing anything to do with health benefits is a confidential and possibly sensitive subject. Do not divulge any personal medical information, or talk about specific claims or medical issues.

You can discuss the merits of keeping the benefits plan sustainable, and how that can be achieved.

How to Achieve a Sustainable Benefits Plan

Employers can utilize the below plan design options to help with the overall cost of an employee benefits plan.

- Cost-Sharing: For businesses that use a cost-sharing arrangement, employees also have a stake in keeping the premium costs reasonable.

- Co-Pay: Adding a co-insurance or co-pay percentage to the group insurance plan can also help to mitigate the costs for the plan sponsor.

- Deductibles: Including an annual or per prescription deductible can further reduce costs if needed.

- Stop-Loss: Including stop-loss protection means any claims incurred above the specified dollar amount will be the responsibility of the insurer rather than the employer. This is especially important when high-cost drugs or chronic medical issues are a factor.

- Disability Management Program: Having a Disability Management Program can help mitigate the incidence rate of disability claims.

- Employee Assistance Program (EAP): An EAP can also help reduce the incidence rate for mental health disability. It can also help in other areas, such as providing financial guidance before the stress becomes too much to bear and the employee requires time off.

Even if employees are not paying part of the premiums, if a plan is no longer sustainable, employers will need to cut costs somewhere. Employees may lose some coverage they are used to having if costs are unmanageable.

Employers should encourage their employees to utilize their group insurance plans, but be aware that maximum utilization from every employee is not sustainable. Be conscious of your running claims experience. Ensuring employees’ understanding of how the benefits plan works can go a long way to achieving a sustainable benefits plan.