Grading our 2024 predictions for group health insurance trends

By: Benefits by Design | Tuesday February 18, 2025

Updated : Monday June 15, 2026

Our 2024 predictions were thoroughly investigated, and upon reflection and further research, we’re pleased to present our findings. How well did we do for each prediction, and why?

In case you missed them, or you need a refresh, here’s the original blog post:

A deep dive into health insurance trends and predictions for 2024

Prediction #1 – Chronic diseases will have a big impact on the workforce

“With the rise in chronic diseases, as well as the further acceptance of obesity as a chronic disease, we believe employers will see this impact health insurance trends and therefore their benefits plans in 2024.”

According to the 2024 Benefits Canada Healthcare Survey (BCHS), the prevalence of chronic diseases increased to 58% of plan members in 2024, up from 54% in 2023. Depression, anxiety, or other mental health conditions represented the highest number of cases, at 22% of all chronic conditions.

At the same time, 9% of plan members reported having diabetes – a disease which often comes with congruent illnesses such as high blood pressure, chronic obesity, and even depression.

However, there was some reprieve. The large increase that occurred in 2023 of off-label use of GLP1 and semaglutide diabetes medications has mostly been mitigated. Although the data isn’t quite out yet, we expect there was a decrease in the overall amount claimed for diabetes medications in 2024.

Lastly, access to care has continued to decrease. In fact, 22% of Canadians report not having a family doctor – compared to 14% in 2022. Combined with increasing wait times for treatment by a specialist, this means that many Canadians forego treatment altogether. This can exacerbate conditions and creates higher medical bills in the future.

Grade: All things considered, we’re very happy with our 2024 prediction. However, we’re giving ourselves minus two points on this one for the decrease in diabetes medication spending.

Prediction #2 – Financial concerns will continue to be the biggest cause of employee stress

“Until inflation and interest rates settle or decrease, we expect to see financial concerns as the main cause of employee stress throughout 2024. This will likely affect other health insurance trends as utilization of services to combat stress goes up.”

Inflation was a major concern in 2024, despite its steadying in the latter half of the year. However, the increase in prices on everything from groceries and gas to rent and car payments did not go down, which means that Canadians are still feeling the effects.

Retirement savings continues to be a concern as well. According to the People Corporation Next Paper: Retirement outlook in Canada, 54% of retirees reported carrying debt into retirement (including mortgage debt), and 43% are concerned they won’t have enough savings to make it through retirement. Another 24% have continued working past retirement, 31% of those because they need the income.

The October 2024 TELUS mental health index did a special report on financial well-being, which revealed that 40% of workers often feel worried or anxious about their financial situation.

Finally, 43% of plan members ranked personal finances as their number one source of stress in the 2024 BCHS. Not surprisingly, 54% of those with poor financial health also reported high levels of daily stress.

Grade: We’re tooting our own horns and giving this one a perfect score!

Prediction #3 – Employers will not be immune to financial concerns

“The question, ‘how do employers provide higher coverage maximums while maintaining cost-containment?’ will be a focus for the group insurance industry in the coming years. Look to see plan updates that include higher annual maximums and increased frequency limit amounts, while paring back unused benefits to keep costs reasonable. We also expect the continued health insurance trend of adding healthcare spending accounts to benefits plans to provide further coverage and flexibility.”

Last year saw the employer struggle between providing robust benefits versus affordability continue in full force. In fact, by popular demand, we updated our stop loss options to include higher thresholds at slightly lower fees. Providing employers with the option to take on slightly more risk for reduced fees.

The BCHS also found that employers have indeed increased their coverage maximums for paramedical services. In 2023, the average annual combined maximum was $1,364, whereas in 2024 it was $3,353.

Despite this, inflation took its toll, and employees spent an average of $1,172 out-of-pocket for healthcare expenses that went over their coverage maximums. This divide between coverage and need can cause significant damage to the real and perceived value of the employee benefits plan. Not to mention plan member health. In fact, 27% simply discontinue treatment and wait until plan maximums reset the following year.

In terms of health care spending accounts, the BCHS surveys show that increased slightly as well, from 38% of plan sponsors indicating they have one in 2023, to 40% in 2024.

Grade: Employers did indeed shell out for higher maximums and spending account access. However, it was hard to find evidence of paring back, so we’re giving ourselves minus one point.

Prediction #4 – Mental health and wellness – the continuing saga

“We predict there will be a slowdown in workplaces prioritizing employee mental health and wellness. As the shift in stigma continues, employers may see this as a sign that their employee benefits are hitting the mark. And if they are, we agree there is no reason to fix something that isn’t broken. We expect to see continued health insurance trend of wellness benefits utilization, as indicated by the continual rise in spending on mental health support year over year.”

Mental health and wellness certainly continued to be a hot topic in 2024! However, we believe digital wellness programs had more time in the spotlight than did mental health counselling, prescription drugs for mental health issues, and disability leaves due to mental health issues. Even though the latter three are the biggest cause of disability claim prevalence and costs.

Again, we found data in the BCHSs. Among plan sponsors that cover mental-health counselling separately, the average annual maximum in 2024 was $1,743. By comparison, it was $82 higher the year before. Add that to the fact that 82% of plan members who are heavy users of mental health benefits said the “coverage level limited their ability to seek necessary treatment”, and it’s clear the mental health epidemic is still very much here.

If the above does not already indicate high spending on mental health support, the rise in the use of anti-depressants also supports this.

Grade: We think we did a pretty good job predicting this one as well. We’re giving ourselves minus two because while mental health benefits utilization continues to rise, it’s not necessarily inclusive of all wellness benefits. Plus, we weren’t expecting the annual maximums to decrease.

Prediction #5 – Benefits communications will become more innovative

“As the world becomes increasingly more dependent on technology, it will surely help us communicate group benefits in a more personal, concise, and easy-to-understand way.”

There was a lot of talk about benefits communication in 2024, and some strides were made. However, overall, employees still do not understand their benefits as much as we would like them to.

One study found that 49% of professionals are unsatisfied with employee benefits communication. And the 2024 BCHS found that only 47% of employees understand their benefits extremely or very well.

The challenges are these:

- How do we communicate complicated information in an easily digestible format to an audience that isn’t interested?

- How do we ensure that when they are interested because they need the benefits, they know where to go to find information on their benefits?

- How do we make sure they understand enough so they are aware when they are eligible to receive benefits?

At the same time, 55% of employees indicated their preferred method of communication is email. Which does not align with the anecdotal evidence we’ve been hearing about employees wanting customization.

Grade: This trend doesn’t appear to have flourished in 2024 as much as we expected. The group insurance industry still has a long way to go in terms of communications, but we did take a big step forward in the conversation, which is the first hurdle. \

Prediction #6 – Artificial Intelligence will be incorporated to some degree

“There may be more of an opportunity [for AI] behind the scenes: the integration of AI into application development and maintenance. We also expect to see more use of AI for data analytics, benefits fraud detection, and risk management.”

We saw a lot of discussion around AI in 2024, and a lot of innovation and progress was made. Internally, AI helped save time during application development, as well as data analyzation and exploration for risk management.

It also helped save time in content development for emails and explanations of complicated results or policies.

AI has been found to be the most useful in helping with fraud detection, with it’s ability to scan large sets of data for patterns swiftly, and detect anomalies that a human could easily miss. It can also help with real-time claims monitoring.

Grade: We’re giving ourselves good marks for this one. AI is being used by a lot of advisors in day-to-day applications, and it has been useful in the three areas we predicted. Minus one point since it’s not as far along as we believed it would be.

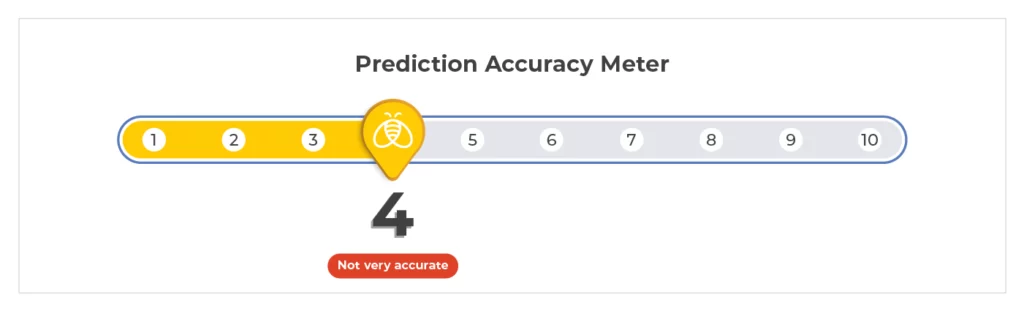

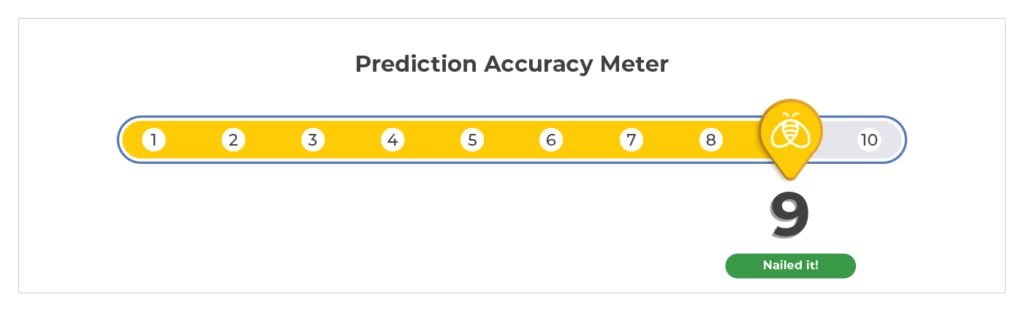

All things considered; our 2024 predictions turned out to mostly hit the mark. We had a grand total of 48/60, or 80% accuracy.