In Canada, there are many methods of accessing healthcare — provincial health care plans, group insurance plans, and individual insurance plans, for a start.

Yet when it comes to individual and group health insurance, there are some key differences working Canadians should be aware of. Let’s start with the definition of each:

Group Health Insurance

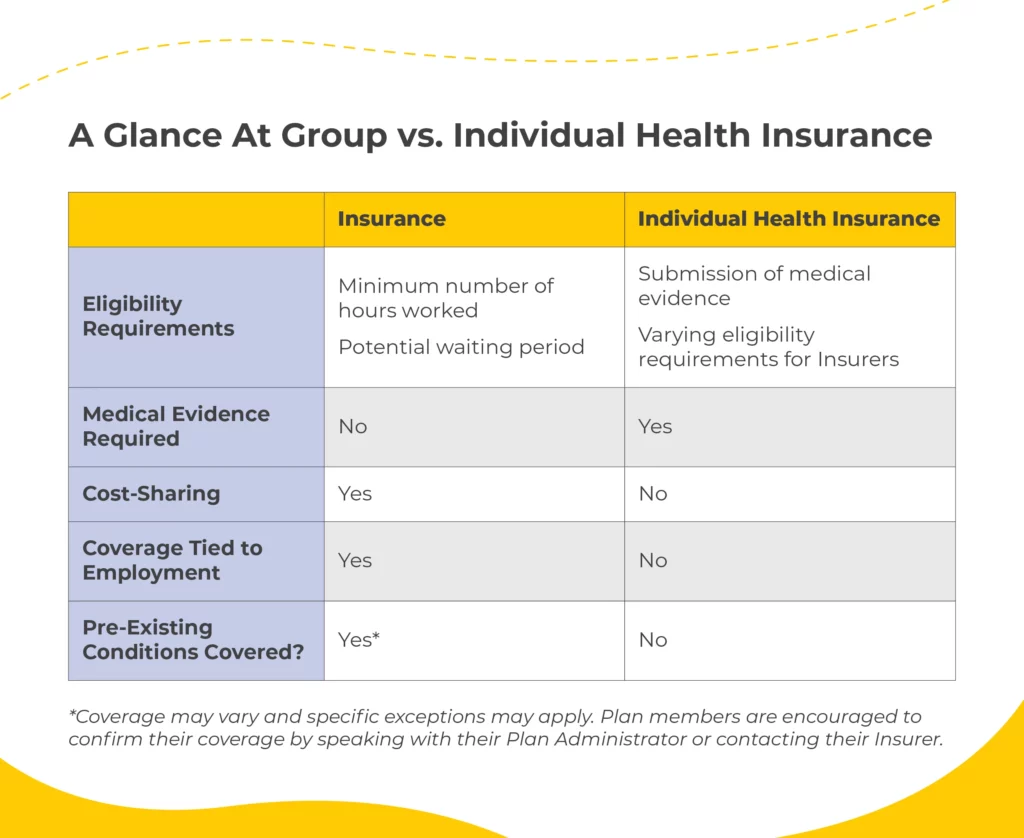

Group health insurance is provided to employees through their employer. Eligibility for employees under a group insurance plan is very straightforward. It is typically based on the number of hours worked and after meeting a waiting period. Employees who apply for group coverage as a late applicant may have a more difficult time, which is why applying for coverage on time is so important! These plans are also set up based on the average age of employees, the industry they work in, as well as the assumption that working employees are generally healthy.

Individual Health Insurance

Individual health insurance is purchased by an individual who requires health coverage above and beyond what the government will cover. These plans are set up based on the individual person’s age, medical condition(s), family medical history, and other lifestyle circumstances. As such, you may be required to submit medical evidence.

What’s Different?

Here, we’ll highlight the most important differences between group health insurance and individual health insurance.

Eligibility and Medical Evidence

With group insurance, individuals do not have to supply medical evidence and are automatically eligible for coverage, provided they work the minimum number of hours and satisfy the waiting period. This makes group insurance very accessible.

Individual health insurance will often require applicants to submit medical evidence and other information prior to approving the coverage (though not all plans). Based on the supplied medical evidence, there is potential for coverage to be denied, whereas this is not the case with group insurance.

Coverage for Pre-existing Conditions

When applying for individual health insurance, the Insurer may deny coverage for any pre-existing conditions (or deny coverage altogether), based on the supplied medical evidence. Individuals with previously documented health conditions, such as diabetes or cancers, may be able to get health insurance, but likely not for those pre-existing conditions. A person’s age and smoking status can also impact coverage and even the cost of coverage.

However, group insurance coverage is available to all eligible employees, regardless of pre-existing conditions. Importantly, this does not necessarily mean that a group plan will offer coverage for all pre-existing conditions, as there may be specific pre-existing condition clauses within group insurance.

For example, travel insurance generally requires that a person is in stable condition for a certain number of days prior to departure. This is usually somewhere between 30-90 days.

What is Travel Insurance and What Do I Need to Know Before Travelling?

Another example of this is Disability Insurance. Claims may be denied for a condition that was treated within a certain time frame prior to coverage, and for which is claimed within a certain period of time after coverage commences. For example, if a person was treated for chronic back pain within 3 months of their coverage effective date, and then made a claim within 12 months, they may be denied. However, if they make their claim after the 12 months, this would not be an issue. These time frames vary by policy, always check with your insurer or plan administrator to confirm these details.

Cost Differences Between Group and Individual Health Insurance

As a general rule, group insurance will cost a person less than individual insurance for the same or comparable coverage. This is the case for three reasons.

- One — in group insurance, the risk of a claim is spread out across a large number of persons who are considered healthy (employees in a workplace). This is known as risk pooling.

- Two — in group insurance, employers are required to pay a minimum of 50% of the premiums for most benefits. Special consideration is made for Disability Insurance, as there are tax implications depending on who pays the premium. More on that below.

- Three — the cost of group insurance benefits is taken from an employee’s before-tax paycheque. With individual health insurance, you’ll pay premiums with after-tax dollars.

With individual insurance, the entirety of the premium cost is on the individual without employer cost-sharing. Additionally, premiums are paid with after-tax dollars rather than before-tax income. All of this is added to the fact that individual insurance premiums are typically quite expensive for robust coverage.

Everything Employers Need to Know About Group Insurance Underwriting

Policy Termination

For group insurance, insurance coverage is tied to the covered person’s employment. This means that coverage begins after they have satisfied a waiting period, and coverage will cease if that person leaves their job for any reason. Coverage may be extended (such as for a retiring employee or as part of a severance package), but only for so long, and it is still dependent on the last day of employment of the individual. For employees who are losing their group coverage, they have the option to convert their benefits to individual coverage. In this case, the medical evidence that would normally be required is waived.

Employment does not affect the termination of individual health insurance policies as they are purchased separately by a person who requires the coverage. This is not to say that their job might not be a factor in what type of coverage they need or are able to receive. For example, sports athletes require different coverage than an office worker, and the price for coverage may also vary.

Continuation of Benefits for Leaves of Absence, Layoffs, and Retirees

Tax Implications: Group Health Insurance vs. Individual

Premiums

For group insurance, the employer is able to add the premiums they pay for their employees coverage to their business expenses. In other words, it is a tax write-off. For Life, AD&D, Disability, and Critical Illness benefits, the amount of premiums the employer pays is considered taxable income for the employee. Extended Health Care, Dental, and EAP premiums are exempt from this and are not added as taxable income for the employee.

Shared premium costs are deducted directly from the employee’s pay, which means they are using pre-tax dollars to pay for their premiums.

For individuals purchasing individual insurance, they would be using post-tax dollars. These premium amounts can be claimed as a medical expense on the individual’s personal income tax return.

Benefits

When it comes to claiming the benefits, there are also tax implications. For medical and dental expenses that are covered, these cannot be claimed as individual medical expenses, as the employee has been reimbursed. The amount that is reimbursed to the claimant should also not be added as income to the individual tax return.

For Life and AD&D benefits, the benefit received by a beneficiary is non-taxable. This is not dependent on who paid the premiums for the insurance coverage.

Disability insurance is slightly different. If an employer pays the premiums, the benefit amount received by the claimant is taxable. If the employee pays the premiums, the benefit amount is non-taxable. For this reason, many group disability plan premiums are paid 100% by the employees. Again, because the employee is using pre-tax dollars to pay the premiums, savings are still realized over an individual plan.

While there are reasons to have both types of coverage, generally speaking, if your employer has group coverage, it is advantageous to enroll. In some cases, enrollment may even be mandatory (this is especially true for small to medium sized businesses). Plus, if you do end up leaving the specific company under which benefits are provided, they are responsible to advise employees of their conversion options for continued coverage.