How did we do in terms of the accuracy of our trends and predictions for 2023? There are a lot of moving parts within the group insurance industry – and all of them work in tandem to create a mosaic of employee health and wellness support and services. Looking ahead helps us stay focused on what’s important. And it helps the group health insurance industry continue to collectively improve.

Let’s take a look at how well we did with our predictions last year:

1. Delayed care due to COVID-19 will cost plan sponsors and plan members

Our prediction: “Overall, plan members’ health has suffered, and will continue to suffer as we play catch-up with our healthcare system. Their out-of-pocket expenses for co-pays will likely increase, since medical costs continue to rise with inflation, and cost sharing may increase as a result of increased premiums.”

We looked at medical trends to see if inflation is affecting medical costs. According to the Aon’s Annual Global Medical Trend Rates reports, in both 2019 and 2020, Canada’s medical trend rate rose by 6%. However, in 2023, that increased to 7.5%. This means that inflation had a bigger impact on medical expenses in 2023 than in previous years.

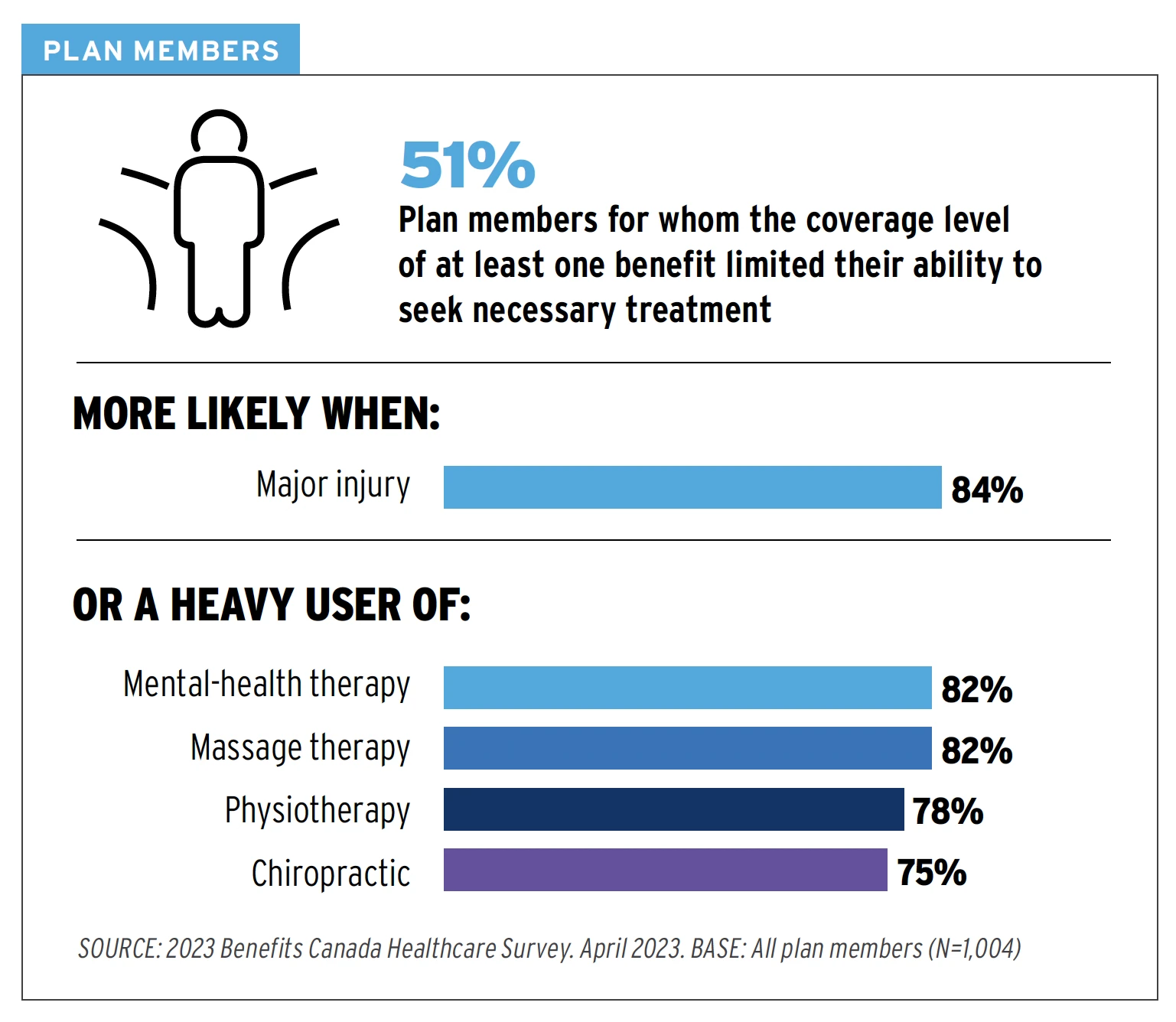

That impact was felt by plan members. When it came to out-of-pocket expenses, more than half of employees had benefit plan maximums that were not adequate to provide necessary treatment. For those with an injury or who required mental health therapy, that number went up to 82% or more. (See image below)

The 2023 Benefits Canada Healthcare Survey (BCHS) reported employees’ out-of-pocket expenses were an average of $3,515 – growing to $5,158 for those between age 18-34.

Finally, increased overall premiums due to inflation meant that cost-sharing for employees also increased. Since 50% of a larger amount will always be a larger number.

Score: 10/10 – nailed it!

2. Mental health and wellbeing initiatives still have a ways to go

Our prediction: “We expect to see more mental health and wellness benefits and innovations being explored and implemented in the coming year.”

Companies leaned into their mental health initiatives and goals in 2023. As stigma continues to dissipate, employers put their money where their mouth was and actively added programs.

Highlights from the 2023 BCHS around mental health and wellness show this to be true:

- 61% of plan sponsors offer mental health support;

- 73% of plan sponsors offer a wellness program (of which 48% include mental health services);

- 77% of plan members agree their company culture encourages health and wellness – rising to 85% when virtual care is included, suggesting that innovative technologies are helping;

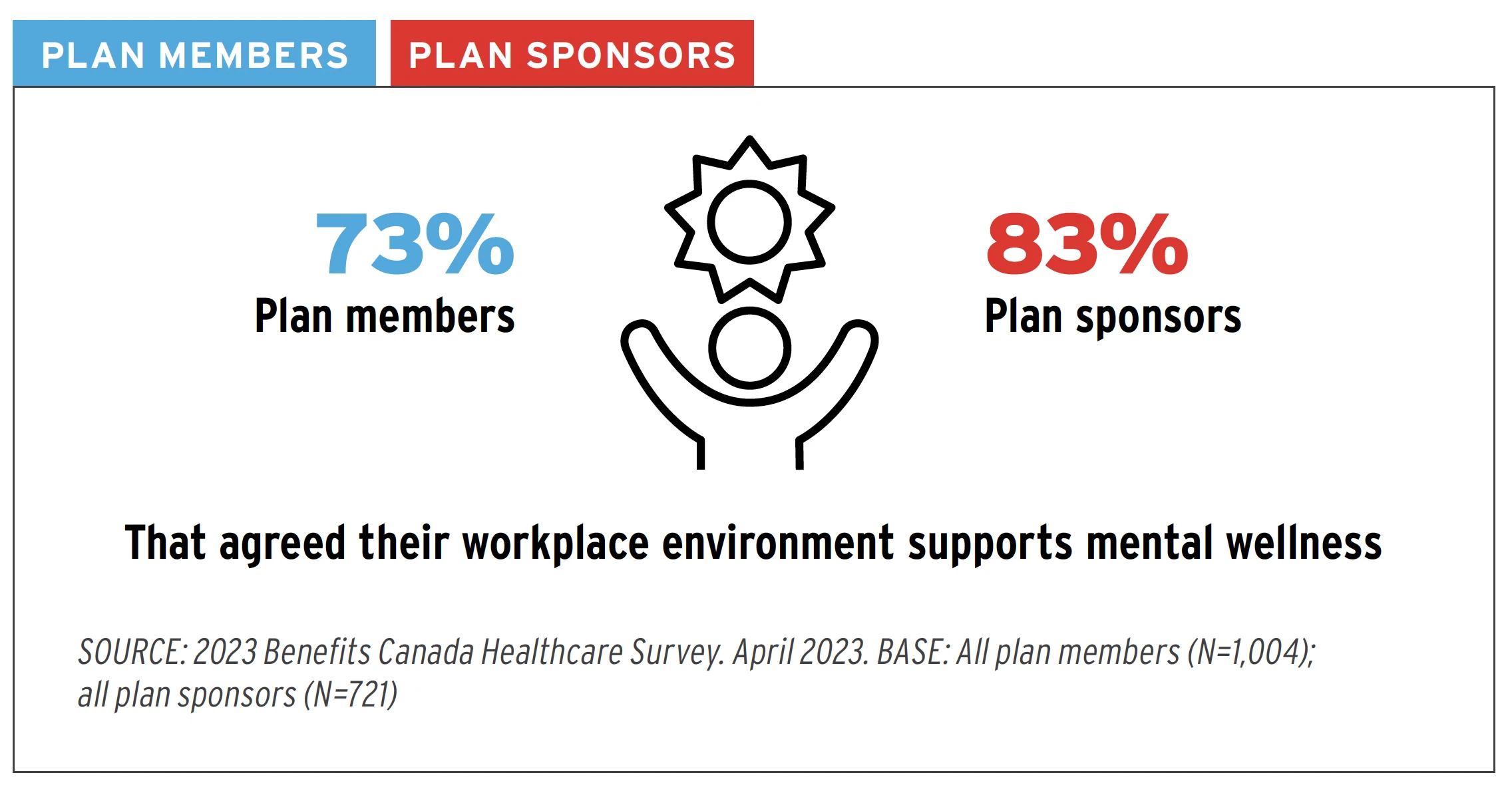

- In 2023, only 27% of employees did not agree their workplace environment supported mental wellness (see image below). This is a marked improvement compared to the previous year. In 2022, 77% of employees felt the help they got from their employer to manage their mental health was only somewhat or not effective.

The Aon global wellbeing report suggests that plan sponsors are adding more services and solutions, but more needs to be done to increase utilization of these benefits and programs.

The North American results show the disconnect:

- 70% of plan sponsors say wellbeing is more important than in 2020;

- 52% of plan sponsors increased spending on wellbeing support, however, only 32% say their wellness programs perform well.

Score: 8/10 – minus 2 points because plan sponsors did well to add more benefits, but inadequate communication has led to less than desirable usage of these benefits.

3. Mental health disability claims will keep going up

Our prediction: “Given the current state of the Canadian health care industry, claimants will most likely continue to take longer to return to work. This may be impacted more greatly by returning to the office as employees struggle with adapting to the new (old) way of working.”

Disability claims for mental health continued to increase in 2023 as Canadians continue to grapple with the after-effects of the pandemic. That, combined with the decrease in mental health stigma, has led to more people making disability claims for mental health. And these types of claims tend to cost more than claims for other conditions. This is because the duration for mental health claims is often longer, and the treatment is varied, multi-faceted, and often faces trial-and-error periods before getting the desired results.

According to the Canada Life Claim Trends and Cost Drivers Report, there was an overall increase in claims for mental health conditions for both long- and short-term disability (STD). In fact, mental health claims made up 26% of all disability claims and represented 33% of the total amount paid to plan members.

The jury is still out on the mental health effects of the return to the office. A lot of companies did not implement policies until later in the year, and there was some pushback from employees. We’ll check back later to see how employees are coping with back-to-the-office work mandates.

Score: 9/10 – minus 1 point due to the mental health effects of the return to the office not quite being felt yet.

4. High-cost drugs will continue to be the main factor in health plan increases

Our prediction: “Unsurprisingly, high-cost drugs are still expensive, and this doesn’t appear to be changing anytime soon. We also predict that other provinces will look at implementing a biosimilar substitution program in the coming year(s).”

The Express Scripts Drug Trend report showed an increase of 6.3% spending on prescription drugs, mostly driven by an increase in claimants, rather than an increase in the amount each one claimed.

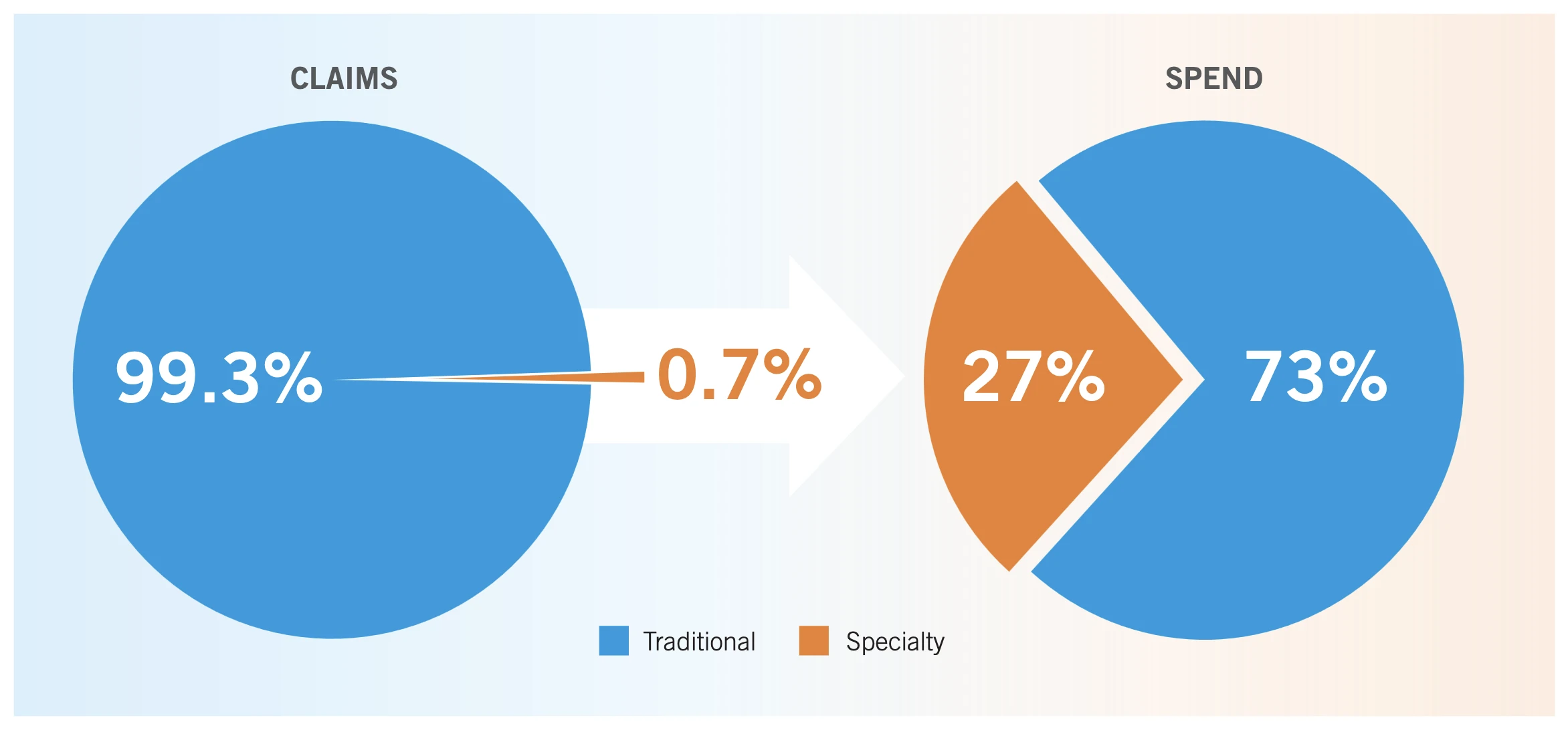

Surprisingly, the increase was larger for traditional drugs than it was for high-cost drugs. However, high-cost drugs still represent 73% of the total amount reimbursed, while only representing 0.7% of the claims. (see image below)

Again, the 2023 BCHS reported that 88% of plan sponsors feel more could be done to reduce the burden of specialty drug costs on employer sponsored drug plans. What’s more, 77% agreed (27% strongly) they are concerned about their plan’s ability to continue covering higher-cost drugs.

Our own block of business saw an almost 20% increase in claims above the $10,000 stop-loss threshold. Meaning reimbursement for specialty drug claims increased, resulting in higher stop-loss fees.

Biosimilar programs have been implemented in both Saskatchewan and Ontario after the success of similar programs in other provinces. We won’t be surprised if more provinces and territories follow suit soon.

Score: 8/10 – minus 2 points because high-cost drug trend increases were slightly less than traditional drug trend increases.

5. Inflation will impact claims experience and plan designs

Our prediction: “We think we’re going to see large increases at renewals in 2023. And there could be lots of plan design changes or marketing of groups as well.”

We already know that inflation had an impact on the out-of-pocket expenses for plan members. And the 2023 BCHS had even more statistics to help confirm our prediction.

- 49% of plan sponsors agree the most important benefits plan improvement is to increase coverage levels to keep pace with inflation;

- 14% of plan sponsors reported removing or reducing benefits or coverage levels, double the amount from 2022 (7%). This was to help mitigate the increasing costs due to inflation of benefit plan premium.

We looked at the number of plan amendments we completed in 2023, and there was a 5% decrease from the previous year. However, 2022 saw an abnormally high amount of plan amendments, so we still saw a large number of plan design changes overall.

Our overall claims experience for health and dental also saw a slight decrease from last year. We believe this is because the surge in back-logged dental and medical claims we saw in 2022 slowed down somewhat.

Score: 7/10 – minus 3 points for the fact that inflation did not have as big of an impact as we thought it would specifically on claims experience and plan design changes.

6. Remote and hybrid work will continue to prompt updates and innovation

Our prediction: “Even though many offices are full of life once more, the best practices that we adopted in order to let everyone work from home should continue to shine and make our work more efficient.”

Overall, the accuracy of our trends for this prediction was almost 100%.

The 2023 BCHS found that the number of employers (29%) who provided virtual health-care services was unchanged from the previous year.

However, the addition of online support through newer technologies did increase according to the Gallagher 2023 Workforce Trends Report:

- 89% have a payroll system;

- 72% of Canadian employers have some form of HR technology strategy;

- 59% use a human resources integration system (HRIS);

- 43% offer virtual counselling services;

- 38% provide telemedicine services.

All of this means that employers are continuing to use the new efficiencies, online tools and virtual connections that were adopted over the previous three years.

Score: 9/10 – minus 1 point since telehealth services did not see as big an increase as expected, and since not all employees have the option for paperless benefits enrollment – yet.

7. Diversity, equity and inclusion initiatives will bloom

Our prediction: “Watch for lots of discussions surrounding DEI benefits, and plan design updates as employers race to be more inclusive.”

Diversity, equity and inclusion (DEI) was a hot topic in 2023. But was it just performative? According to a Gallagher 2023 Workforce Trends Report, employers are walking the walk.

A whopping 78% of employers have DEI recruiting standards that they apply. And 47% of companies indicated the main purpose of their DEI initiatives is to align with their organizational core values. Indicating this won’t just be a flash in the pan trend.

Meanwhile, the same report shows that 22% of companies have integrated DEI initiatives into their employee benefits plans, a trend which we hope to see continue.

GreenShield added Gender Affirmation coverage in December 2022 – an inclusive benefit which provides coverage for foundational and focused surgeries that help with the physical transformation for people with gender dysphoria. We saw less than 5% of our groups opt out of the coverage.

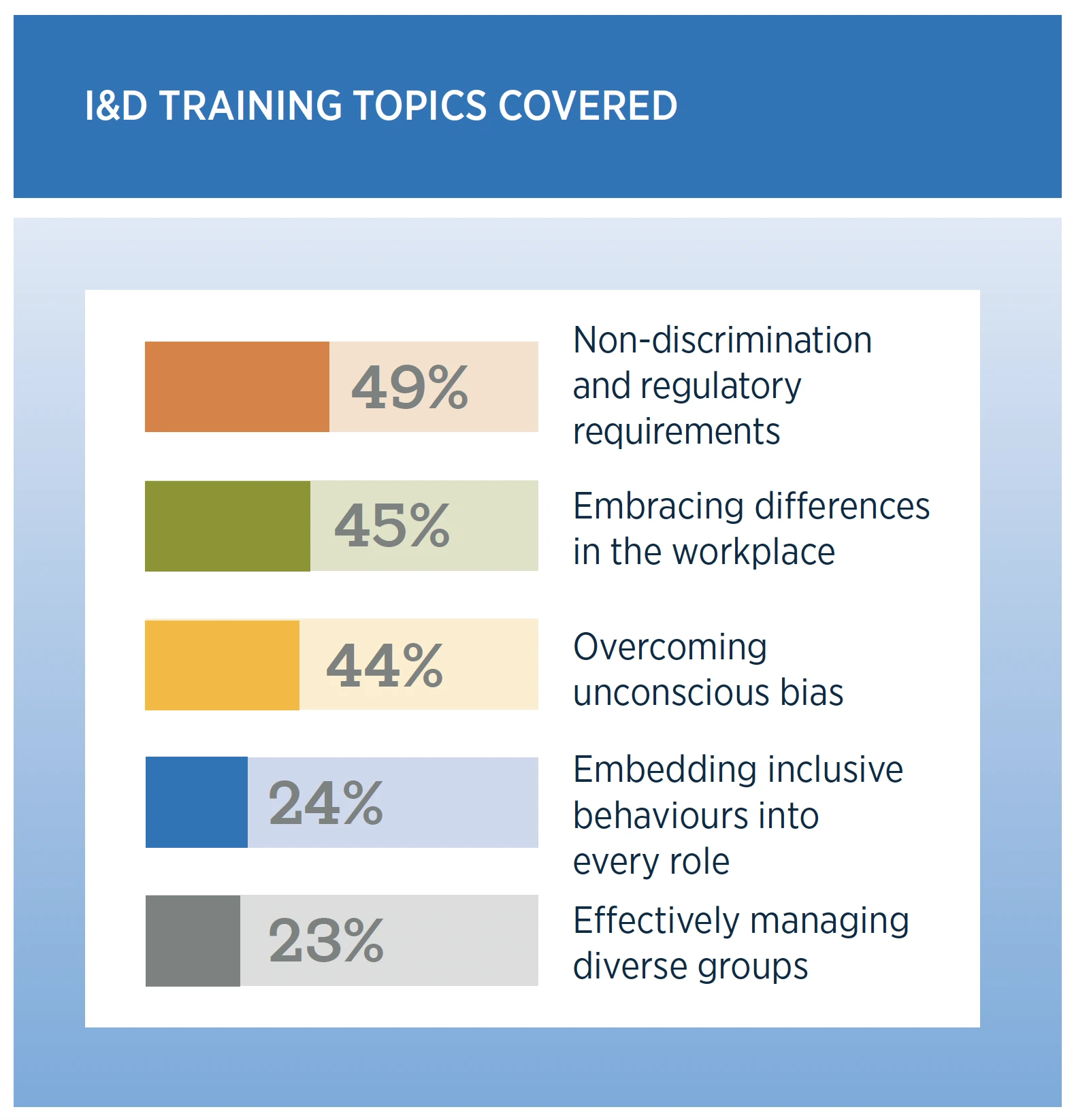

Lastly, the Gallagher report also showed the inclusion and diversity (I&D) training topics that companies offered in 2023. The following image confirms employers’ commitment to improving DEI within the workplace:

Score: 9/10 – minus 1 point because we couldn’t confirm plan design changes were made or not made for more inclusivity outside of our own block.

8. Retirement and Termination Ages Could Get a Makeover

Our prediction: “Insurance companies will need to start looking at termination ages to match plan sponsors’ work forces. The reduction of insurance that occurs at age 60 and 65 for Life Insurance and accidental death and dismemberment (AD&D) could be seen as a form of ageism, and insurers may need to adjust to ensure equal treatment of all demographics.”

Workers over the age of 55 now make up more than 20% of the workforce – the highest percentage ever for this demographic. Canadians are also retiring 3.4 years later than they used to, and only 6% are working beyond the usual retirement age because they enjoy it. On the flipside, some retirees are unwillingly coming back to the labour force, or working multiple jobs, just to stay afloat.

Yet insurers and providers still have some catching up to do. New ideas will need to be explored to help cover older employees’ health needs.

We’ve seen minimal plan design changes to this effect, with the exception of a few groups adding separate extended health coverage for employees over 70. This is mainly due to the higher fees for travel insurance for these employees.

We have not seen any changes to the reduction in the benefit amount for life insurance and accidental death and dismemberment (AD&D) insurance.

Score: 3/10 – minus 7 points because we believe this trend is moving much slower than we anticipated.

9. Change to Employment Insurance Sickness Benefit Length

Our prediction: “Given the fact that most LTD claims stay open for longer than the extension, we’re predicting that there won’t be a marked decrease in LTD claims. Initial speculation is that there would be a decrease in LTD rates should employers choose to extend.”

We did not receive requests to update the long-term disability (LTD) elimination period to match the new Employment Insurance (EI) sickness benefit duration. Nor did we see a noticeable decrease in LTD claims. And since there wasn’t enough data, it is unclear whether the rates for LTD would decrease if the elimination period is extended.

As expected, there was a higher frequency of mental health disability claims last year, which means the accuracy of our trends and predictions was almost spot on!

Score: 9/10 – minus 1 point for not having the data to confirm a decrease in rates.

Conclusion

We scored a total of 72/90 points, which gave us 80% on the accuracy of our trends and predictions for 2023. Not exactly an A performance, but we’ll take the B+.