Coordinate your health and dental care plan with your health care spending account [Free infographic download]

By: Benefits by Design | Tuesday March 26, 2024

Updated : Tuesday April 22, 2025

Giving employees flexibility and choice in their benefits plan is more important than ever. Not only because of the heated war for talent, but also because there are currently five different generations in the workforce. Employers can protect themselves against high-cost claims while providing robust coverage when they coordinate your health and dental care plan with your health care spending account (HCSA). Plus, employees who may not use their benefits as much can recoup some of their health and dental premiums.

Coordinate your health and dental care plan with your health care spending account

Employees with access to both insured health and dental as well as a HCSA have the ability to maximize their HCSA allotments. It is important to submit any medical or dental claims to the insured plan first. Then, any amounts not covered by that plan, can be submitted to the HCSA for reimbursement.

What You Need to Submit Medical Claims Under a Group Insurance Plan

We’ve outlined a variety of scenarios where this might be useful.

When the fully-insured plan has co-pay or coinsurance

Co-pay means each claim is only reimbursed at a percentage of the total. Meaning, if the plan pays 80%, the employee is left paying 20% out-of-pocket. The employee can then submit the 20% to their HCSA for reimbursement.

When the employee has reached their annual maximum

Certain services or medical equipment have annual maximums to keep costs contained. For example, there could be a $500 annual maximum for physiotherapy. Once that maximum has been reached, the employee can submit subsequent visits under their HCSA for reimbursement.

When the employee has reached their frequency limits

Other services are offered based upon how often they are required, such as vision care. For example, many plans provide coverage for eye exams once every two years. If an employee were to get an eye exam before that time, they could submit it to their HCSA.

When the employee has coverage through an individual or spousal plan

The same options as outlined above are also available if the employee is covered for health and dental by an alternate plan. Claims should be submitted first to the employee’s plan, then to the individual or spousal plan, and lastly to the HCSA.

For more information on coordinating two fully-insured plans, check out our blog post explaining all the details: Coordination of Benefits: Can I Have More Than One Benefit Plan?

Paying premiums

Lastly, not all employees will use the entirety of their allocated HCSA dollars. In that case, they can submit their fully-insured premiums for health and dental as a medical expense under the HCSA. Thus, they aren’t leaving money on the table, and they pay less money out-of-pocket for the cost-sharing of benefit premiums.

List of Health Care Spending Accounts (HCSA) Eligible Expenses

Submitting partial claims to your HCSA

When submitting a claim for a partial amount, it is imperative to provide the HCSA adjudicator with the information they need to confirm the reimbursement amount. Any claims that are reimbursed through an insurer will come with an explanation of benefits (EOB). This document should accompany any receipts submitted to the HCSA so they can confirm which amounts were already covered.

It is considered fraud to submit a claim twice for the full amount, once for reimbursement via the fully-insured plan, and then again under the HCSA. This is why it is so important to include the EOB.

The biggest rule to remember when you want to coordinate health and dental coverage with a HCSA is that claims need to be submitted under the fully-insured plan first. Even if the claim is denied, the EOB shows the HCSA adjudicator that it was not covered by the insurer, and therefore it is eligible for coverage under the HCSA.

Provide your employees with an easy-to-follow infographic on how it all works

Download the infographic: Coordinate your health and dental care plan with your health care spending account (PDF: 705 KB)

Coordinate your health and dental care plan with your health care spending account

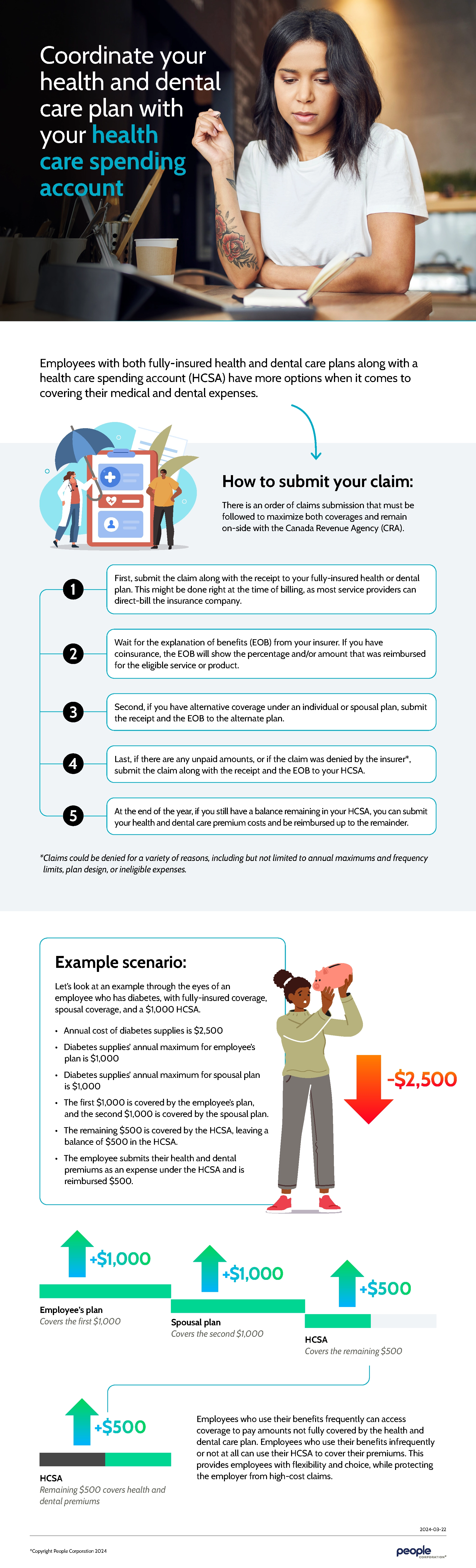

Employees with both fully-insured health and dental care plans along with a health care spending account (HCSA) have more options when it comes to covering their medical and dental expenses.

How to submit your claim:

There is an order of claims submission that must be followed to maximize both coverages and remain on-side with the Canada Revenue Agency (CRA).

- First, submit the claim along with the receipt to your fully-insured health or dental plan. This might be done right at the time of billing, as most service providers can direct-bill the insurance company.

- Wait for the explanation of benefits (EOB) from your insurer. If you have coinsurance, the EOB will show the percentage and/or amount that was reimbursed for the eligible service or product.

- Second, if you have alternative coverage under an individual or spousal plan, submit the receipt and the EOB to the alternate plan.

- Last, if there are any unpaid amounts, or if the claim was denied by the insurer*, submit the claim along with the receipt and the EOB to your HCSA.

- At the end of the year, if you still have a balance remaining in your HCSA, you can submit your health and dental care premium costs and be reimbursed up to the remainder.

*Claims could be denied for a variety of reasons, including but not limited to annual maximums and frequency limits, plan design, or ineligible expenses.

Example scenario:

Let’s look at an example through the eyes of an employee who has diabetes, with fully-insured coverage, spousal coverage, and a $1,000 HCSA.

- Annual cost of diabetes supplies is $2,500

- Diabetes supplies’ annual maximum for employee’s plan is $1,000

- Diabetes supplies’ annual maximum for spousal plan is $1,000

- The first $1,000 is covered by the employee’s plan, and the second $1,000 is covered by the spousal plan.

- The remaining $500 is covered by the HCSA, leaving a balance of $500 in the HCSA.

- The employee submits their health and dental premiums as an expense under the HCSA and is reimbursed $500.

Employees who use their benefits frequently can access coverage to pay amounts not fully covered by the health and dental care plan. Employees who use their benefits infrequently or not at all can use their HCSA to cover their premiums. This provides employees with flexibility and choice, while protecting the employer from high-cost claims.