Researching, quoting, implementing, and onboarding an employee benefits plan is just the start of the group insurance journey. Understanding your coverage isn’t always easy, which is why Insurers provide a Schedule of Benefits, summarizing coverage. But even that can be confusing when it’s your first time with benefits, so let’s dissect one piece by piece.

What is a Schedule of Benefits?

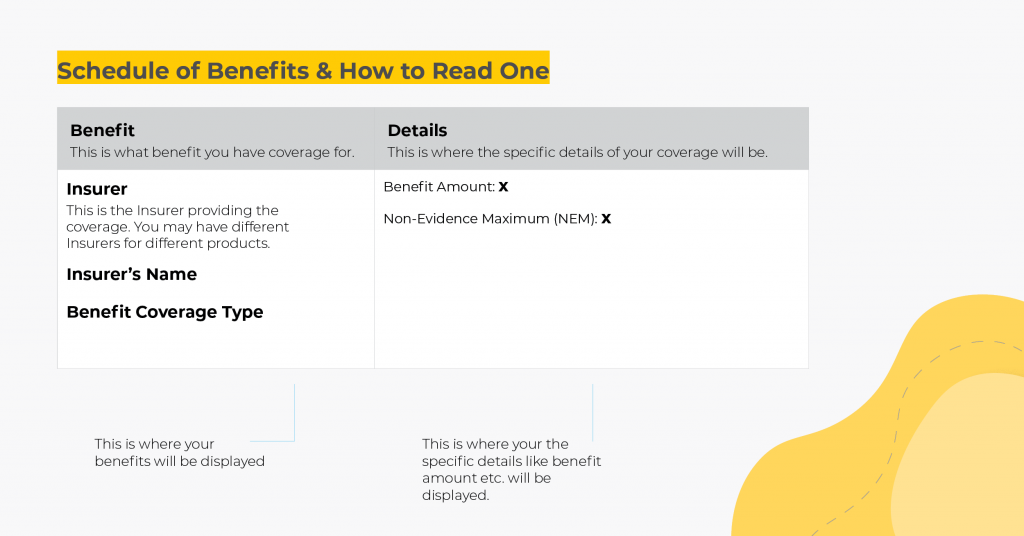

Your Schedule of Benefits is a summary of the benefits included in your employee benefits plan. It lists each benefit, any applicable maximums, termination ages, and percentages at which claims are covered. It’s an excellent resource to learn more about your coverage and is typically provided at the beginning of an Employee Benefits Booklet.

Group Health and Dental Insurance Specifics Every Employee Should Know

Although it does not include all of the pertinent information regarding your benefits plan, it does provide a summary of the basics of your coverage. Let’s take a look at the basics of a Schedule of Benefits before we “zoom in” on specific benefits.

[Free Download] How to Nail Your Benefits Communication Strategy

How to Read the Schedule of Benefits

For this exercise, we’re going to take a closer look at a typical Schedule of Benefits for our own Starter Plan, which by default includes the following coverages:

- Extended Health Care (EHC), including prescription drug, paramedical coverage, and Travel Insurance

- Dental Insurance

- Life and Dependent Life Insurance

- Accidental Death and Dismemberment (AD&D) Insurance

This information is being used as an example only, and coverages, percentages, maximums, and other information may vary by Insurer. Employers and employees both are encouraged to contact their Plan Administrator or Insurer for specific information regarding their plan.

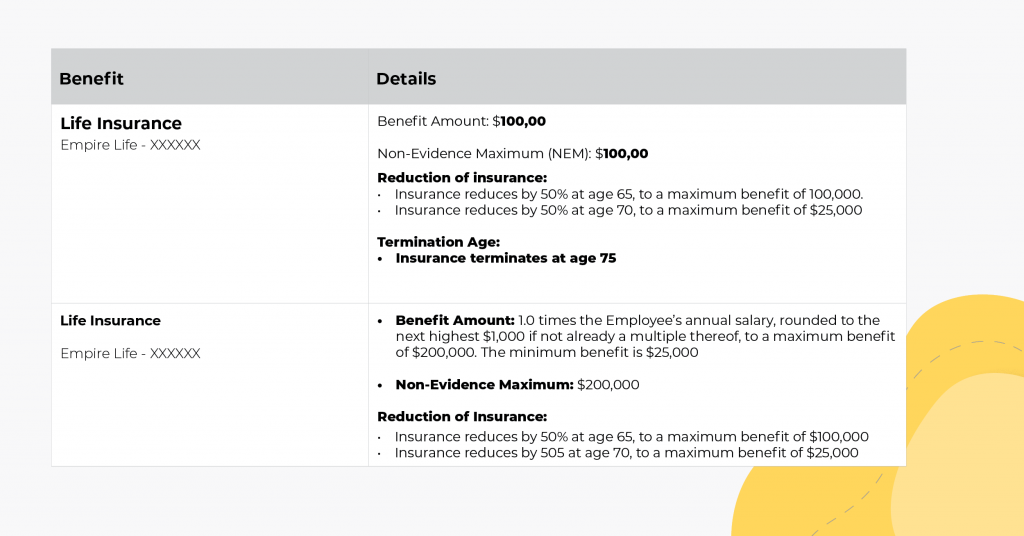

Life Insurance:

When it comes to Life Insurance, there are two common methods of paying out a benefit: either as a lump-sum payment (ex. $100,000) or as a multiple of earnings (ex. $50,000/year x 2 = $100,000).

We’ll look at both below:

In either case, the Benefit Amount shows the amount provided to the designated beneficiary, either as a lump sum (Image 1), or as a multiple of salary (Image 2). Your Schedule of Benefits will clearly outline how your Life Insurance benefit is calculated. In cases where the benefit is delivered as a multiple of salary, you’ll also see a minimum and a maximum benefit stated.

Your Non-Evidence Maximum (NEM) is the maximum amount of coverage you can access without providing further medical evidence to your Insurer. Eligible employees will be able to apply for additional coverage beyond the NEM and Plan Administrators are required to inform eligible employees about this possibility.

Your Reduction of Insurance outlines the ages and percentages in which your Life Insurance benefit is reduced, while your Termination Age shows you when the benefit terminates.

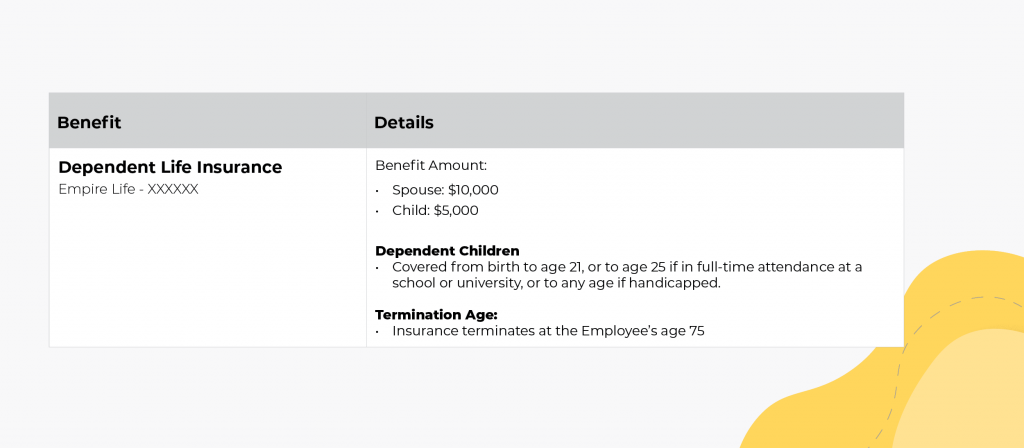

Dependent Life

For Dependent Life Insurance, things are much simpler. The Benefit Amount is what is paid to the beneficiary, which is automatically the employee.

Next we define Dependent Children. For the BBD Starter Plan, for example, dependent children are covered up until the age of 21. Afterwards they lose coverage if they are not enrolled in full-time attendance at a school or university, with the exception of dependent children who are disabled.

The Termination Age here means the same as above. However, it is important to note that this refers to the age of the employee, not their dependents.

Dependent Life Insurance – What is it, and Should You Have it?

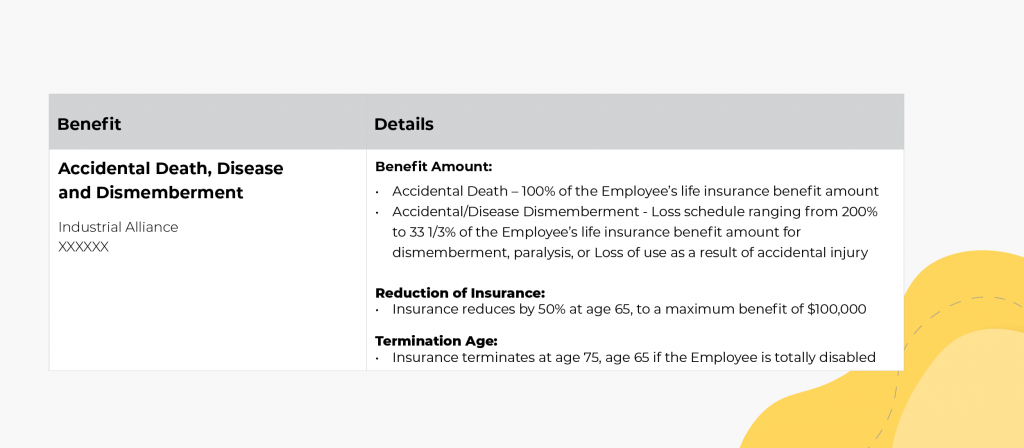

Accidental Death and Dismemberment (AD&D) Insurance

In most cases, the Benefit Amount for an Accidental Death will be the same as your Life Insurance. Should an employee die as a result of an accident, such as a car accident, their beneficiary could receive both the Life Insurance and the Accidental Death benefit.

The other benefits mentioned here, Accidental Disease/Dismemberment and Critical Disease, will vary in amounts, based on the loss (total paralysis provides more benefit than the loss of a finger, for example). The Employee Benefits Booklet will provide further details as to these payments under the Accidental Death and Dismemberment (AD&D) Insurance section.

The Reduction of Insurance and Termination Age for AD&D generally match your Life Insurance benefit.

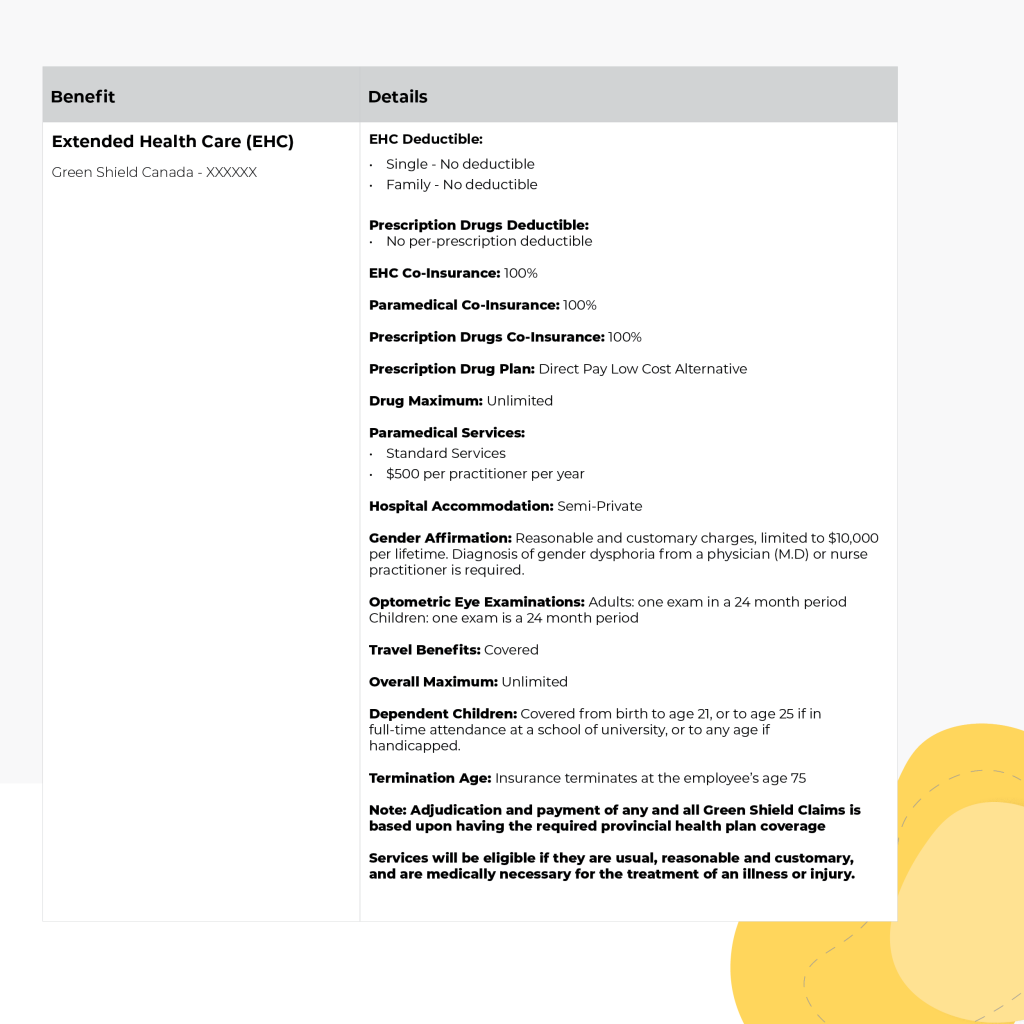

Extended Health Care (EHC)

This is the big one, so bear with us. In this example, Extended Health Care (EHC) contains prescription drug, paramedical, and Travel coverages, so there’s a lot to talk about.

The EHC Deductible may be a familiar concept to you, as it works very similarly to car insurance, with the exception that the deductible is per year instead of per claim. In this example, there is no deductible, but if there were, it would need to be paid out-of-pocket by the employee before the plan begins to cover expenses.

The Prescription Drugs Deductible is paid on each prescription purchased, and can be in addition to the EHC Deductible.

A Coinsurance is the percentage of the bill the Insurer will pay. A common coinsurance is 80% (meaning the employee pays the other 20%), or 100% covered by the Insurer. Coinsurances can vary based on the different types of medical expenses, as depicted above with paramedical and prescription drugs.

The Drug Maximum is the annual limit that an employee can claim for prescription drugs. Subsequent claims for prescriptions beyond this limit would not be covered until the maximum resets with the start of a new Benefit Year.

Paramedical Services refers to medical expenses such as physiotherapy, massage, counselling, or chiropathy. The maximum allowable amount covered will be stated here. In this case it is $500/year, per practitioner, but combined maximums for all practitioners is possible, too. Paramedical services are usually covered only up to a point, which is referred to as “usual, reasonable, and customary”. Each Insurer’s amount covered under this will vary, but the intent behind it is to establish what a “reasonable” expense is. As with the Drug Maximum, this annual maximum for these services will reset with the start of a new Benefit Year.

Hospital Accommodation will cover the cost of an applicable room if a covered employee is in the hospital for any reason. This coverage will be for either a semi-private or private hospital room, and the Schedule of Benefits will dictate what, if anything, is covered.

Optometric Eye Exams refers to the length of time between covered eye exams, and is expressed in what is known as “plan limit frequency”. For example, this Schedule of Benefits offers both adults and children one covered eye exam every 24 months.

The Overall Maximum is the allowable amount of all combined claims for a single employee. This Overall Maximum is for the entirety of their coverage, and can be unlimited (as in this example), or may be set to a specific amount, such as $5,000,000.

Dependent Children will be defined under the Schedule of Benefits, indicating the age to which dependent children are covered, as well as the overage dependent limit for children attending a post-secondary institution full-time.

Termination Age indicates the age at which coverage terminates, and is based on the employee’s age, not the age of their spouse or dependent children.

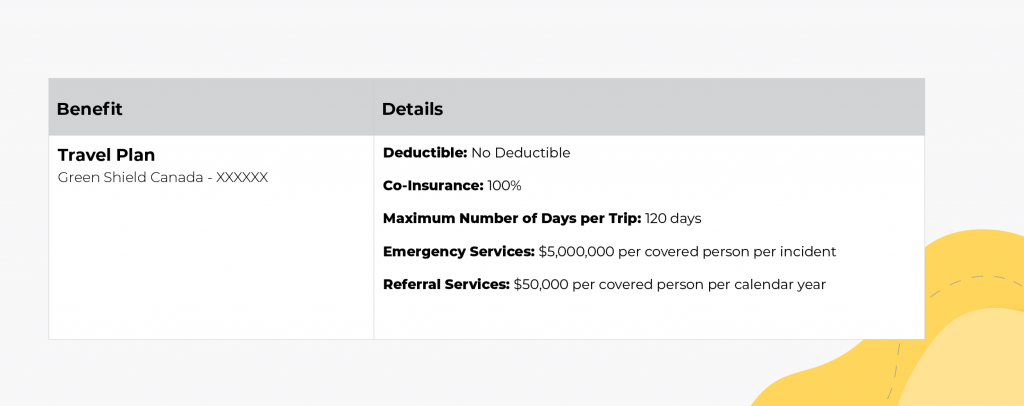

Travel Insurance

The explanations of the Deductible and Coinsurance remain the same as above, so we’ll not reiterate them here.

The Maximum Number of Days per Trip refers to the continuous number of days you would be covered for when travelling out-of-province or out-of-country. If you plan on travelling for longer than this maximum and wish to remain covered, you would need to purchase additional Travel Insurance.

Emergency Services shows the maximum amount that would be paid for each covered person, per claim. If you reach this maximum during one trip, and then travel again months later, you would have access to this maximum again. The exact definitions of what qualifies as “emergency services” and specific coverages will be provided in detail under the Travel Insurance section of your Employee Benefits Booklet.

Referral Services is the maximum that you could claim for a doctor’s referral to have medical treatment done outside of your home province. Referral Services are only considered when there is no path to treatment where you currently reside, but treatment is available elsewhere, such as a highly specialized surgeon.

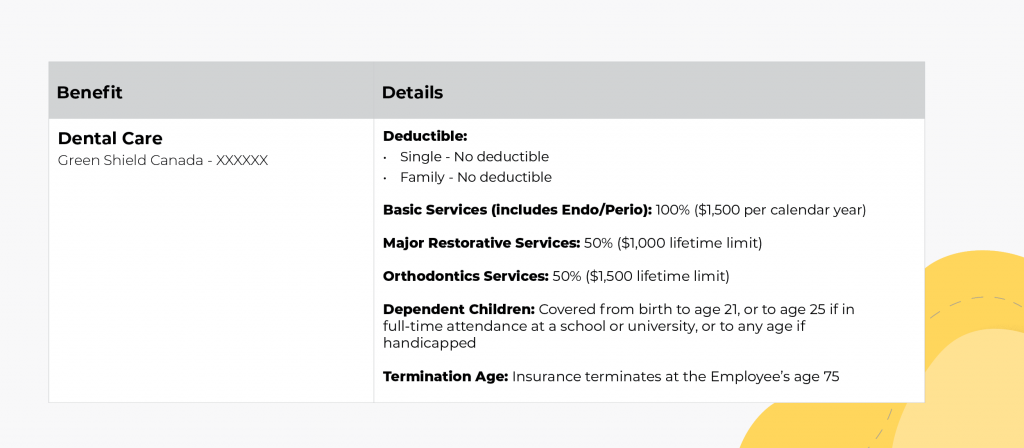

Dental

In this example for Dental Insurance, there is no Deductible. If there were, it would be listed here, and would be the amount the employee must be out-of-pocket before the plan will begin to cover expenses.

Under Basic Services and Major Restorative Services, you will be shown the coinsurance percentage, which is the amount the Insurer will cover, as well as the maximum for claims reimbursement per calendar year. It’s common for coinsurance amounts to be between 80% to 100% for Basic Services, and 50% to 60% for Major Services, though this will vary. Any maximums reset with the start of a new benefit year.

The Orthodontic Service section, which includes things like braces, will show you the coinsurance and maximum for claims reimbursement. The maximum is not combined, and is usually a lifetime limit instead of an annual maximum. A common coinsurance we see for this is around 50% to 60%.

Recall Exams refers to your typical services, like cleanings or x-rays. In this case, the frequency covered is twice a year, with the amount resetting at the beginning of a new benefit year.

Reading a Schedule of Benefits Isn’t Easy

Reading the Schedule of Benefits can be a daunting task, especially if you aren’t sure what some of the terms are specifically referring to. With this basic guide, we’ve broken down some of the more common inclusions, but you should always check with your Plan Administrator or Insurer to confirm your specific coverage.