Why Do We Have Cost-sharing Arrangements for Employee Benefits?

By: Benefits by Design | Tuesday August 22, 2023

Updated : Monday March 23, 2026

Cost-sharing arrangements for employee benefits are a tool that can be used by employers to achieve several outcomes. These can include cost-savings, tax purposes, and employee understanding. Let’s take a look at what cost-sharing is, and then we’ll dig into why we have it.

What is cost-sharing?

“Cost-sharing is the division of responsibility for premium payment between an employer and an employee.” How much each party will pay is determined by the employer upon plan set-up. The most common being a percentage, usually 50%. However, employers can also choose to set a specific dollar amount that employees pay each month, instead of a percentage.

The cost-sharing can also be set up differently for each benefit line. For example, the employer can pay:

- 100% for life insurance and other pooled benefits (such as accidental death and dismemberment or critical illness) and employee assistance program (EAP) premiums;

- 50% of the extended health and dental care premiums; and

- 0% of the disability premiums.

The employee paid portion of the premium is achieved through payroll deductions from the employee’s paycheck. In this way, employees do not pay taxes on those amounts.

It’s important to keep in mind that the portion of premiums that the employer does pay may or may not be taxable to the employee.

Find out more: Download the Group Benefits Taxation Info Sheet

Why do we have cost-sharing arrangements?

One might think, since employers get a tax break on any monies they pay towards employee benefits, and it’s an attraction and retention tool, why would employers implement a cost-sharing arrangement in the first place?

Well, there are several different reasons employers may choose to include cost-sharing for their employee benefits plans. And the reasons can vary depending on the type of benefit.

The Cost of Employee Benefits – Sustainable Plans vs Cheap Ones

Extended health and dental care

When it comes to extended health and dental care, the most common reason for cost-sharing is to help employees understand the value of their benefits plan. Cost-sharing ensures staff understand the total cost of their benefits plan and use benefits wisely.

It also helps them be more involved in and informed about what benefits are included. And how usage can affect the benefits plan premiums at plan renewal.

There are other tactics employers can use to achieve this as well. When combined, they can be a powerful tool towards helping employees understand their benefits plans.

Achieve a Sustainable Benefits Plan Using Your Claims Experience Data

Life insurance and other pooled benefits (excluding disability)

The majority of employers pay 100% of these premiums. This is because the cost is nominal, and the taxation of the benefit received should an employee make a claim is not affected by who pays the premium.

However, if employers do pay the premium, that amount is considered earnings, and the employee is taxed on that amount. Therefore, employers often set up a 50/50 split to offset this.

Lastly, as with health and dental, this arrangement can help with employee understanding of the value of their benefits plan.

Any optional pooled benefits premiums are paid for 100% by the employee.

Short-term and long-term disability

Taxation of disability premiums are in a world unto themselves. These are the only benefits where the party who pays the premiums directly affects the taxation of the claimed benefit.

- If the employer pays any portion of the premium, the benefit received by the claimant (employee) is taxable.

- If the employee pays 100% of the premium, the benefit received by the claimant (employee) is non-taxable.

The second option is far better in the long run if an employee is collecting disability payments. It means that the entire amount is theirs to use. And they will not be taxed on those payments as earned income.

If disability premiums are being split or paid in full by the employer, the percentage of an employee’s income they would receive as a claimant is usually higher. For example, a non-taxable plan usually provides an employee with 66.67% of their weekly or monthly earnings. While a taxable plan would usually provide around 75%.

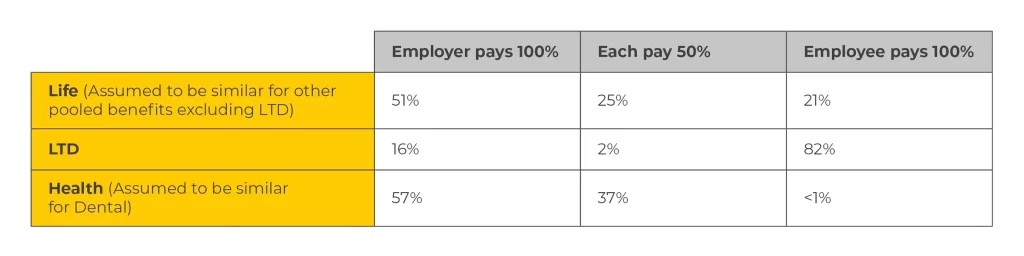

A look at BBD’s average cost-sharing arrangements by benefit line

We took a look at our own block of business to get an idea of what Canadian employers are setting up for their cost-sharing arrangements.

The figure below shows that the majority of employers pay for life insurance and pooled benefits, as well as extended health and dental care.

Unsurprisingly, 82% of employers with long-term disability plans have set them up to have 100% of the premiums paid for by the employee. Thus, allowing the benefit to be non-taxable.

Employee benefits are a huge factor for employees when assessing their current or future job situation. And with the tight labour market, it may be tempting for employers to pay for it all to entice top talent. We hope that reading this has provided a clearer understanding of the benefits of cost-sharing arrangements – both for the employer and employee.